Toastmasters en Español

July 29, 2026

New Orlando Regional REALTOR® Association data shows Central Florida home sales increased for the fifth month in a row as the summer market heats up.

ORRA’s full State of the Market Report for June can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, Lake and Volusia counties by members of any REALTOR® association, not just members of ORRA.

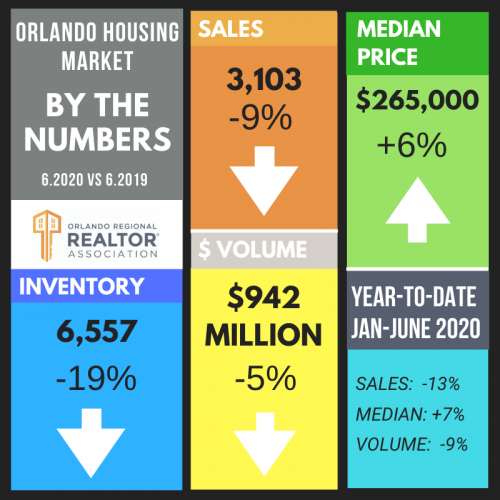

New Orlando Regional REALTOR® Association data shows rise in sales heading into summer season.

ORRA’s full State of the Market Report for May can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, Lake and Volusia counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows sales cooled slightly while new listings increased and prices remained up year over year.

The Orlando Regional REALTOR® Association’s monthly housing reports are now reflecting residential real estate activity across Orange, Osceola, Lake, Seminole and Volusia counties.

ORRA’s full State of the Market Report for April can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, Lake and Volusia counties by members of any REALTOR® association, not just members of ORRA.

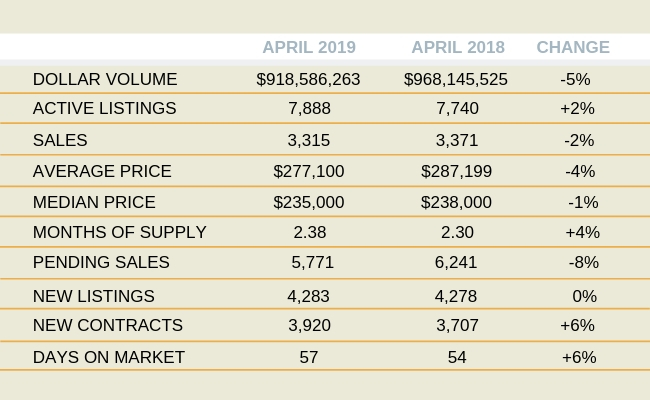

New Orlando Regional REALTOR® Association data shows rise in sales and new listings, signaling a strong spring market.

ORRA’s full State of the Market Report for March can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows interest rates drop back into 5.0%-range.

ORRA’s full State of the Market Report for January can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows spike in new listings to kick off the year.

ORRA’s full State of the Market Report for January can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Regional REALTOR® Association releases overall 2025 data, revealing a steadier, more balanced market with prices holding at record highs and sales moderating amid higher rates.

(Cumulative 2025 totals compared to cumulative 2024 totals)

ORRA’s full State of the Market Report for December can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows slowdown in sales and listings as the market shifts toward the holiday season.

ORRA’s full State of the Market Report for November can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows interest rates continuing to trend down.

ORRA’s full State of the Market Report for October can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows lowest interest rates in a year.

ORRA’s full State of the Market Report for September can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows a drop in sales, inventory, and new listings as Orlando continues to shift to a buyer’s market.

ORRA’s full State of the Market Report for August can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month June be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

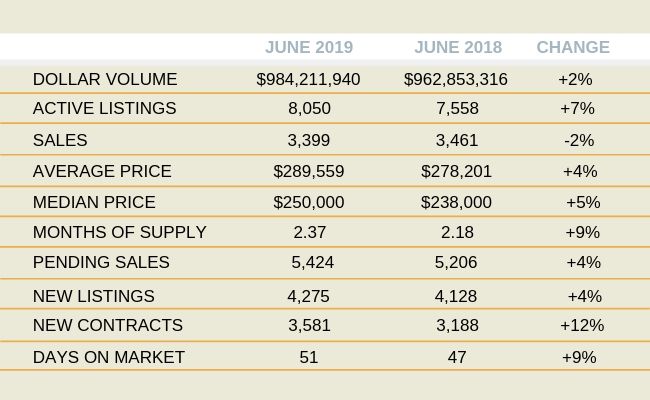

New Orlando Regional REALTOR® Association data shows interest rates reach lowest level this year.

ORRA’s full State of the Market Report for June can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month June be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows a drop in new listings as some Orlando sellers pull out of the market.

ORRA’s full State of the Market Report for June can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows nearly 14,000 homes on the market heading into busy summer season.

ORRA’s full State of the Market Report for May can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows strong sales and inventory as market heats up.

ORRA’s full State of the Market Report for April can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows rise in sales and pending sales as winter winds down.

ORRA’s full State of the Market Report for February can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows spike in new listings to kick off the year.

ORRA’s full State of the Market Report for December can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Regional REALTOR® Association releases overall 2024 data, revealing demand for homes held strong as inventory rose and buyers adjusted to higher interest rates.

(Cumulative 2024 totals compared to cumulative 2023 totals)

ORRA’s full State of the Market Report for December can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

You can find ORRA's full State of the Market Report for May here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows a balanced market for the first time since February 2011.

ORRA’s full State of the Market Report for October can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows break in nine-month streak of rising inventory.

ORRA’s full State of the Market Report for October can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows highest inventory in nearly ten years.

ORRA’s full State of the Market Report for September can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for August 2024

New Orlando Regional REALTOR® Association data shows interest rates reached a two-year low

State of the Market

Market Snapshot

Inventory

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows market continues to stabilize for homebuyers as inventory increases for seventh month in a row.

You can find ORRA's full State of the Market Report for May here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows inventory surpasses 10,000 homes for first time since 2016.

You can find ORRA's full State of the Market Report for May here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows record-high median home price in Central Florida real estate housing market.

You can find ORRA's full State of the Market Report for April here.

This information comes from the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy.

Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Because of late closings, we need to make changes to include sales posted after our reporting date. We need to make changes because of late closings.

These changes will include sales posted after our reporting date. ORRA REALTOR® sales are sales made by members of the Orlando Regional REALTOR® Association. These sales are mainly in Orange and Seminole counties, but can also occur in other areas.

Note that we may revise statistics released each month in the future as we receive new data.

The Orlando MSA numbers include home sales in Orange, Seminole, Osceola, and Lake counties. These numbers are not limited to just ORRA members; any REALTOR® association member can contribute to them.

New Orlando Regional REALTOR® Association data shows spike in listings kicking off the new year

ORRA’s full State of the Market Report for March can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows spike in listings kicking off the new year

ORRA’s full State of the Market Report for February can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows spike in listings kicking off the new year

ORRA’s full State of the Market Report for January can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Regional REALTOR® Association releases overall 2023 data, revealing that rising interest rates were the biggest factor affecting housing market in 2023, slowing sales and boosting inventory.

(Cumulative 2023 totals compared to cumulative 2022 totals)

ORRA’s full State of the Market Report for December can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month September be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows inventory spikes as interest rates reach new heights.

ORRA’s full State of the Market Report for September can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month September be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows inventory spikes as interest rates reach new heights.

ORRA’s full State of the Market Report for September can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month September be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows rates reach highest level in over 20 years, contributing to market slowdown this fall.

ORRA’s full State of the Market Report for September can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month August be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for August 2023

New Orlando Regional REALTOR® Association data shows market continues to cool as fall season approaches

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for August can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month July be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for July 2023

New Orlando Regional REALTOR® Association data shows interest rates reach second-highest level in 20 years, impacting Orlando’s housing market

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for July can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month June be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for June 2023

New Orlando Regional REALTOR® Association data shows the highest median home price this year as an uptick in inventory hits the summer market

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for June can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for May 2023

New Orlando Regional REALTOR® Association data shows rise in sales and median home price as summer selling season heats up

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for May can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for April 2023

New Orlando Regional REALTOR® Association data shows rise in inventory and fall in home sales, indicating spring selling season may be balancing out

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for April can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for March 2023

New Orlando Regional REALTOR® Association data shows an increase in new listings and home sales as spring buying season begins

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for March can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for February 2023

New Orlando Regional REALTOR® Association data shows an increase in home sales and median home price heading into spring buying season

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for February can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for January 2023

New Orlando Regional REALTOR® Association data shows lowest number of home sales in nearly 15 years

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for January can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for December 2022

ORRA’s full State of the Market Report for December can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows home sales drop significantly heading into the holiday season

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for November can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively – located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association data shows interest rates reach highest level in over

20 years and how that’s impacting the local housing market

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for October can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for September 2022

New Orlando Regional REALTOR® Association data shows interest rates surge as home sales see biggest drop since January 2022

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for September can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for August 2022

New Orlando Regional REALTOR® Association data shows median home price falls for second consecutive month as homes spend more days on the market

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for August can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for July 2022

New Orlando Regional REALTOR® Association data shows median home price falls for first time in

six months as inventory spikes for the third straight month

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for July can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for June 2022

On the rise: New Orlando Regional REALTOR® Association data shows inventory and home prices make big jumps for the second consecutive month

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for June can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for May 2022

Orlando Regional REALTOR® Association’s May data shows the single biggest monthly surge in Orlando inventory ever

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for May can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for April 2022

Orlando Regional REALTOR® Association’s April data shows interest rates reach their highest levels in more than 10 years, indicating the market could be cooling off as overall monthly sales drop for the second time this year

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market Report for April can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for March 2022

Orlando Regional REALTOR® Association’s March data shows the spring market is in full swing with a surge in new listings and a record median home price; interest rates are also on the rise, hitting their highest point in over a decade

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for March can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Area Residential Real Estate Snapshot for February 2022

New Orlando Regional REALTOR® Association data shows the spring market starting to heat up with a record high median home price, increases in new listings and overall sales

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for February can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Regional REALTOR® Association’s newest data shows interest rates continue to rise at a slow pace while sales decrease

State of the Market

Market Snapshot

Inventory

ORRA’s full State of the Market report can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

Orlando Regional REALTOR® Association releases overall 2021 data, revealing a historic year of real estate in Orlando, including an all-time record low for inventory and an all-time record high for median home price.

2021 Annual Market Recap

(Cumulative 2021 totals compared to cumulative 2020 totals)

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for December can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New data from Orlando Regional REALTOR® Association reveals slowing sales, as median home price continues to climb for seventh straight month

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for November can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New data from Orlando Regional REALTOR® Association reveals slowing sales, as median home price continues to climb for seventh straight month

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for October can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New data from Orlando Regional REALTOR® Association reveals slowing sales, as median home price continues to climb for seventh straight month

State of the Market

Market Snapshot

Inventory

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New data from Orlando Regional REALTOR® Association reveals slowing sales, as median home price continues to climb for seventh straight month

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for August can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New data from Orlando Regional REALTOR® Association reveals slowing sales, as median home price continues to climb for seventh straight month

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for July can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association report shows just three weeks of inventory available, as new listings quickly come under contract

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for June can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association report shows just three weeks of inventory available, as new listings quickly come under contract

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for May can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

New Orlando Regional REALTOR® Association report shows just three weeks of inventory available, as new listings quickly come under contract

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for April can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month of be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association report shows continued squeeze on the number of homes for sale

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for February can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

New Orlando Regional REALTOR® Association report shows continued squeeze on the number of homes for sale

State of the Market

Market Snapshot

Inventory

ORRA’s full Market Pulse Report for January can be found here.

This representation is based in whole or in part on data supplied by the Orlando Regional REALTOR® Association and the Stellar Multiple Listing Service. Neither the association nor StellarMLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or by StellarMLS does not reflect all real estate activity in the market. Due to late closings, an adjustment is necessary to record those closings posted after our reporting date.

ORRA REALTOR® sales represent sales involving Orlando Regional REALTOR® Association members, who are primarily – but not exclusively - located in Orange and Seminole counties. Note that statistics released each month may be revised in the future as new data is received.

Orlando MSA numbers reflect sales of homes located in Orange, Seminole, Osceola, and Lake counties by members of any REALTOR® association, not just members of ORRA.

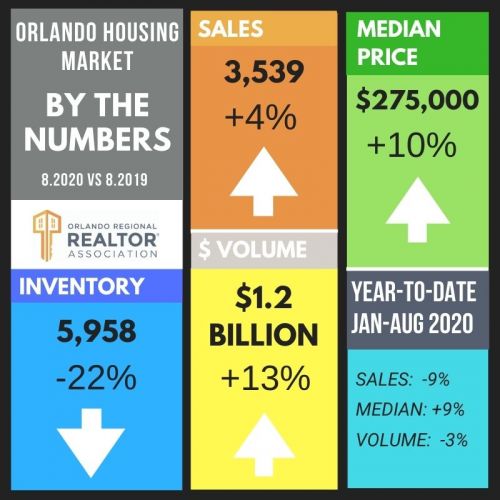

A new report from the Orlando Regional REALTOR® Association details how the housing market fared in 2020 compared to recent years. Despite the pandemic and its impacts, Orlando’s median home price rose as buyers scrambled to find homes in a market with consistently shrinking inventory.

According to the report, Orlando’s annual median home price for 2020 ($265,000) was 9.1% higher than the 2019 annual median price ($243,000), thanks to another 12 months of year-over-year median price increases. While the median home price rose each month, inventory continued to decline and reached a low in December 2020, when it reached the lowest level since July 2005.

Orlando home sales completed during 2020 racked up a final tally of 36,871, which is 0.5% above the cumulative sales total of 36,707 for 2019. For historical comparison, annual sales in 2019 were 1.8% above the cumulative total sales for 2018; yearly sales in 2018 were 3.2% lower than in 2017.

“The Orlando area was red-hot throughout 2020, as demand spiked and the number of houses on the market dropped throughout the year. We expect this pattern to continue in 2021,” said ORRA 2021 President Natalie Arrowsmith, NextHome Arrowsmith Realty. “Looking at the data, inventory has significantly decreased since the beginning of the year. In fact, December 2020 shows the lowest inventory we have seen in more than 15 years, which creates an extremely competitive market for buyers.”

Editor’s Note: Additional 2020 cumulative statistics are included at the end of this release

Median Price

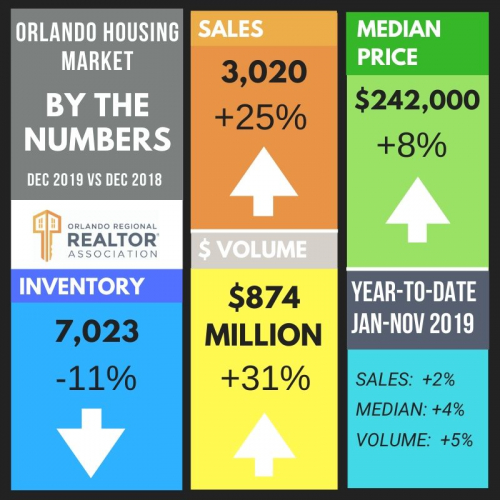

The overall median price of Orlando homes (all types combined) sold in December is $275,000, which is 10.4% above the December 2019 median price of $249,000.

The median price for single-family homes that changed hands in December increased 12.1% over December 2019 and is now $296,950. The median price for condos increased by 5.7% to $148,000.

Sales and Inventory

Members of ORRA participated in 3,672 sales of all home types combined in December, which is 21.1% more than the 3,033 sales in December 2019 and 51.6% more than the 2,422 sales in December 2018.

Sales of single-family homes (2,890) in December 2020 increased by 20.1% compared to December 2019, while condo sales (401) increased 35.9% year over year.

The overall inventory of homes that were available for purchase in December (4,875) represents a decrease of 30.6% when compared to December 2019 and a 12.7% decrease compared to last month. There were 42.6% fewer single-family homes and 12.1% more condos, year over year.

Current inventory, combined with the current pace of sales, created a 1.3-month supply of homes in Orlando for December. There was a 2.3-month supply in December 2019 and a 3.3-month supply in December 2018, showing that inventory has significantly decreased.

The average interest rate paid by Orlando homebuyers in December 2020 was 2.70%, which remains the same as the month prior.

Homes that closed in December took an average of 45 days to move from listing to pending status.

Pending sales in December 2020 are up 20.9% compared to December 2019 and are down 11.4% compared to last month.

MSA Numbers

Sales of existing homes within the entire Orlando MSA (Lake, Orange, Osceola, and Seminole counties) in December were up by 17.5% when compared to December of 2019. Year to date, sales are down 2.8%.

Each individual county’s sales comparisons are as follows:

2020 Annual Market Recap

(cumulative 2020 totals compared to cumulative 2019 totals)

Median Price

The 2020 annual median home price for 2020 ($265,00) is 9.1% higher than the 2019 annual median price ($243,000) and 14.0% higher compared to 2018’s annual median price ($232,500).

The annual median price of single-family homes increased by 9.6% to $285,000 in 2020, while the median price of condos increased by 7.4% to $145,000.

Sales

Sales in 2020 were up by 0.5% over 2019. A total of 36,871 homes were sold in 2020, compared to 36,707 the previous year.

Sales of single-family homes increased by 2.3% over 2019. Condo sales were down 10.2% and townhomes were down 1.2%.

By year’s end in 2020, 40,743 homes were sold in the Orlando MSA whereas 41,922 homes had been sold by year’s end in 2019, for a 2.8% decrease. Each individual county’s year-end sales comparisons are as follows: